Emerging Fund Managers have historically been known to outperform. As far as representation: In the US, women represented 14%, Black and Hispanic represented 3% each, of investment partners. Despite the shortage of diversity, there is a growing fraction of emerging managers representing female and minority groups. What this can mean is different thought processes, more creativity in ideas, and potentially more business value. This ensures Emerging Fund Management is a niche, but interesting topic, which is why in this report we provide an overview of Emerging Fund Managers.

Emerging Fund Managers include Venture Capitalists, which we will refer to in a separate section of this document. However, we would like to mention that since 2015, Venture Capital funds raised in billions have been increasing since 2014, and the number of funds too. Note that the figure 1 was from June 2020, which is not an issue, as it proves our point that fund managers are growing in the number of funds, and the amount of capital raised. Nevertheless, the main point is which of these funds, managed by fund managers actually succeed? Why are investors interested in small funds? This is important since funds have grown, and the number of small businesses, or early stage funds, have grown as a result. This is what we seek to provide an overview towards. It is important to understand the current situation of Emerging Fund Managers, and what defines Emerging Fund Managers, to be able to understand the main ideas of this topic, which is what we do next.

Figure 1: Venture Capital fund count and capital raised

Source: Kauffman Fellows

Statistics

Next, we provide a few statistics. Emerging funds earned an average of 12.2% compared to the overall hedge fund industry of 7.7% – annual figure based on a five year average starting in May 2017. This suggests Emerging Fund Managers generate stronger returns, compared to Hedge Fund Managers. However, there are a few drawbacks, such as during the pandemic, Emerging Fund Managers contributed to only 11.7% of private equity capital raised globally, compared to 18% before the pandemic (year). The figure has been attributed to a 15 year low, but there is good news – some suggest the figure has been attributed to travel restrictions. Does this imply limited partners (LP) pay careful attention to who they support? Is this because 41% of Emerging Fund Managers had less than $25 million in assets under management, therefore a lack of experience? To be able to understand the statistics, it is important to understand what factors strongly influence fund performance, but also what attracts investors to invest towards funds. This is the motivation for the next few topics, or subheadings, of this report. By understanding the subheadings readers should expect to understand the statistics in the field of Emerging Fund Managers.

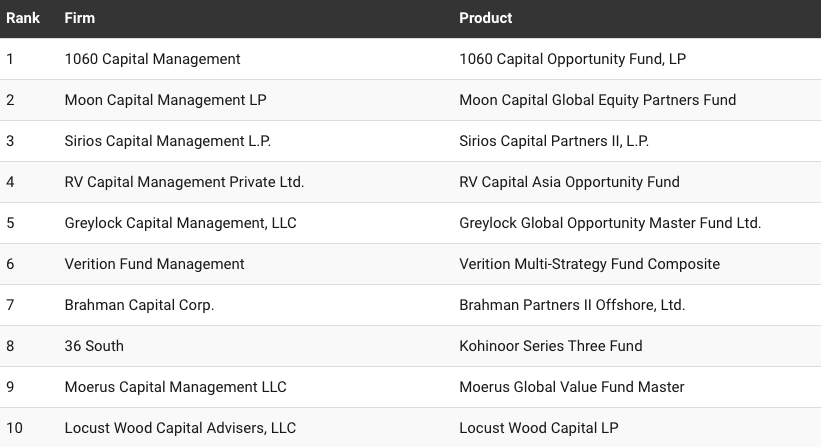

Next, In a research providing the most researched Emerging Fund Managers whose firm has assets managing under $2.5 billion, the following can be noted. Figure 2 demonstrates the top 10 firms, including which of their products is most popular. The next topic of discussion is diversity.

Figure 2: Most researched Emerging Fund Managers

Source: EVESTMENT

Some factors that explain the better performance are technology and social impact driven such those listed in this article. It is in fact becoming a trend to have Emerging Fund Managers, with AON reporting an increase by 11%, from stakeholders to invest in diverse managers. Fund performance may help assess why Emerging Fund Managers are becoming popular. We continue our discussion to the next paragraph.

However, this does not fully support our understanding of the industry. To put this into context, new managers perform better than well established managers, at a significant rate, in their first year. Is this due to investing in technology startups alone? If we assess the technology companies in 2005, it was not until the dot.com bubble that technology companies had grown in value at a significant rate. What this means is ventures can take a while to generate return, strong returns. So, why do new managers perform better than well established managers in their first year, if investments appear to take a long time to generate significant returns? These are the sort of questions we seek to answer.

As part of discussing diversity within Emerging Fund Management, we need to discuss other forms of diversity. Education is one factor influencing the inequality when raising funds, with 43% seed funding distributed to teams with at least one team member that was educated at an elite university. As for racial minorities, only about 2% of VC investors are Hispanic and less than 1% are black. As for the largest VC companies, only 15.7% of the companies have one or more BAME partner. Black investment professionals represented only 3%, and Latin investors reduced by 1% in two years, from 2018 to 2020, from 5% to 4%. There is a strong need for diversity, and we will later find out that during Covid, due to the liquidity strains, it is becoming increasingly important to have diversity for equitable allocation of capital. Next, we analyse capital raised and overall funding activity as part of our discussion of fund management.

Emerging Fund Managers funding activity

Next, as for the overall funding activity we can note the following. In 2017, first time Venture Capital funds reached 31%, a growth of 24% from the 2015 figure. The median net internal rate of return between 2006-2014 for first-time venture capital funds is greater by 3% compared to experienced managers with risk levels 19.1% and 15.6%. Funding counts did not decrease during the pandemic, or 2020. In fact, early stage funding was down by 11% year over year, but up by 5% per quarter, during 2020. What this means is there is not only more capital being raised, but more funding activity during the pandemic too, more specifically for those raising early stage funds. Moreover, 55% more will consider supporting Emerging Managers with funding. The figure of 55% was reported from data collected during the pandemic whilst investors should be more risk averse which is their nature, a basic assumption of economics, yet they are more willing to support emerging managers.

Nevertheless, given the description of the industry, capital raised, and overall funding activity, in the first section, we seek to understand what factors strongly influence fund performance, and in the second section, we seek to understand what attracts investors towards funds. This will help us assess the descriptions stated, but also draw insights.

What factors strongly influence fund performance?

What are Emerging Fund Managers

A formal definition provided by real assets can help us better understand Emerging Fund Managers. Emerging Fund Managers could include managers at an early stage of their investment life cycle, or managers raising a first or second institutional funds, or managers who have a small fund with targeted strategies, or businesses who are BAME (Black, Asian or any other minority ethnicity) and female owned. The definition is crucial to understand the points in the next few sections, or topics, or subheadings, or paragraphs, to be able to explain our main points of discussion.

Next, we seek to understand the qualities of Emerging Fund Managers are driven by performance, and are small firms with big ideas. Due to being a smaller firm, they demonstrate agility compared to their larger counterparts, thereby outperforming larger firms. Due to having big ideas, they have hunger, creativity and the drive to explore alternative solutions. This is the view of 1839 Ventures on Emerging Fund Managers, and a debate is provided in this report. Further they point out investment risk is lessened when there are multiple fund strategies to diversify and spread investment risk. What we learn is that since Emerging Fund Managers find alternative solutions, and are smaller firms or better phrased – smaller funds, which is likely to explain why they outperform their larger counterparts. This is further illustrated in figure 4. Overall this shows, regardless of what defines Emerging Fund Managers, they should possess these qualities.

Figure 4: Fund size and return

Source: real assets

As part of learning about the qualities of Emerging Fund Managers, we need to be able to identify the types of emerging managers. We use information from real assets to help us categorise Emerging Fund Managers. Although these types have been described for real estate, we assume the same types exist for any sort of Emerging Fund Managers, whether they target real estate or not. What supports our assumption is based on a few points on Emerging Fund Manager examples from MITIMCo.

So, the following factors categorize Emerging Fund Managers. First, is the type that has small teams which could be of experienced individuals though not necessary, and wants to launch an initial fund, focused on specific market opportunities, to gain a competitive advantage. Second, is the type who worked well in a previous firm, and launched a new startup partnering with organisations that can benefit from senior managers. Third, is the type of manager with experience in a specific geography. So, we defined, analysed the qualities, and discussed the types of Emerging Fund Managers. Next,we compare Emerging Fund Managers to Diverse Fund Managers, in order to introduce the follow up discussion which is how Emerging Fund Managers can succeed that explains fund performance.

Diversity Stats

Moving forward, for the next few sections the following must be noted. Having a BAME and/or female Fund Manager is important, but much of the discussion of Fund Managers will be based on the categorization of fund managers being smaller firms due to the current evidence at hand. It is only recently, that Diverse Fund Managers are growing, but for now BAME and/or female Fund Managers will be considered as Emerging Fund Managers because they represent 1.3% of total assets under managed, so it is appropriate to classify the category as part of Emerging Fund Managers, as they are managing a small fund.

According to Chicago Booth “the number of funds started by women or by Black or Latinx founders has risen considerably.”

How Emerging Fund Managers can succeed

Emerging Fund Managers have small teams that could possibly be inexperienced. What this means is identifying which Emerging Fund Managers can succeed is important, whether they are inexperienced which is an important factor, or not. So, we delve into minimizing the risk of selecting an inadequate Emerging Fund Manager by providing an overview on how to identify the right Emerging Fund Manager, and therefore identify factors that explain fund out performance which in turn mean successful fund management.

First, Emerging Fund Managers can succeed by identifying and building relationships with investors, limited partners and general partners. To have a good relationship with investors it is important to have a good team, but also manage risk. Having an effective team will demonstrate good company culture, and being able to manage risk is important as most investors are risk averse. Next, to build a good relationship with limited partners and general partners the following can be noted. Limited partners require substantial resources to perform due diligence. For instance the LPA, limited partnership agreement, sets out the advisory fee arrangements, which is paid directly from the fund to the Emerging Fund Manager, it can affect the performance of the fund, and the return for limited partners. In turn, if Emerging Fund Managers have good relationships with limited partners, this would be helpful for general partners in using limited partners’ views to manage day to day management of a firm. So, this will help Emerging Fund Managers succeed. Note we will later explain limited partners and general partners, for now we mention the two concepts, briefly.

Second, the goal is to address problems, with unique and differentiated investment strategies. What this means is a good Emerging Fund Manager can provide additional risk and return diversification in the construction of a global portfolio. An Emerging Fund Manager can provide a unique solution by utilizing geographical advantages, or aligning with economic potential. What this will ensure, is that Emerging Fund Managers are likely to outperform their counterparts, larger firms, due to insightful and unique information, and be a useful tool in having a competitive advantage. This will help Emerging Fund Managers succeed.

Third, another driving factor is to consider the value of investments in a portfolio. What this can help understand is the effectiveness of management, are they investing in portfolios with strong valuations? Are these valuations accurate? An effective valuation policy will ensure transparent and consistent results for investors. An Emerging Fund Manager who seeks to build a good relationship with investors by demonstrating accurate investment valuation is likely to succeed by ensuring their investment meets investor expectations, demonstrating a good track record. In other words, managing investor volatility, means Emerging Fund Managers are meeting investor needs, therefore suggesting their successful management of a fund.

Fourth, Emerging Fund Managers should consider security, investor data integrity and protection, as if it is their own. What this means if investor reputation and risk is changed, this affects Emerging Fund Managers reputation and risk. Consequently, Emerging Fund Managers are increasingly likely to put much careful attention to their portfolio, and to how their business is run. This will mean more effort and hard work into their analysis, and accurate valuation will help ensure Emerging Fund Managers succeed as agreed in the previous paragraph. More to the point, investors are customers, as Emerging Fund Managers need to meet their expectations. Paying careful attention to their business, ensuring accurate valuation will ensure effective distribution of portfolios to generate returns. What this means is better management of a portfolio in generating strong returns. Strong returns is an indicator of a fund out-performance, in other words fund managers successfully managing a fund.

Note, for a more in depth analysis of what factors can help assess the success of Emerging Fund Managers, the report by BDO, is a useful tool, and figure 5 summarises what factors have a positive effect on Emerging Fund Managers, in other words help ensure Emerging Fund Managers succeed. Since, Emerging Fund Managers consist of Private Equity Fund Managers and Venture Capital Fund Managers, we next turn to focusing on Venture Capitalist Emerging Fund Managers.

Figure 5: Factors having the most positive impact on a Emerging Fund Manager

Source: Adobeindd

Nano vs. Micro VCs

Nano VC is a fund focused on seed stage with less than $15 million in size, with managers with limited to no experience, where limited partners are high networth individuals or small family offices, usually co-investing and potentially, if leading a fund, they are in the early stage. Micro VC is a fund assets under management from $25 million to $100 million. Both Nano VC and Micro VC funds manage limited funds.

Next, we can note the following statistics. The number of Nano funds as a ratio of new Micro VC, grew by 43%, from 2014 to 2016. This was driven by two reasons, a new trend of supporting those seeking to add value to investors, and LP’s becoming increasingly reluctant to support inexperienced managers. Since, Nano-VC and Micro-VC both consist of inexperienced managers, Nano – VC supposedly grew since there is less capital being managed, hence less capital will be lost if there is a loss. In fact, in the 10 years to 2018, Nano VC funds grew by 11.3%, while Micro-VC grew by 7.8%, which shows seed and early stage funding is growing. This can be better explained when we consider Micro-VC which is the next part of the discussion.

Micro VC has grown over the years as shown in figure 7. What should be noted, first is that North America accounts for most of Micro VC as seen in figure 6. For instance, Between 2012 to 2019, the number of micro managed venture capital funds has grown by 800%. Reasons for growth is the potential for strong returns for being a start up, in niche markets, with improved outcomes, and that thoughtful venture capital can lead to alpha. What this means is a lot of opportunity, and optimism. As a result, since 2019, newer funds have become more popular in ranking, than well established funds, as suggested in figure 7. As agreed earlier, seed and early stage funding is growing.

Figure 6: Micro – VC and Non-Micro-VC Statistics:

Source: Toptal

Figure 7: Ranking of Funds

Source: Kauffman Fellows

Overall, we need to consider a holistic approach when assessing Nano-VC and Micro-VC. Figure 8 shows both Nano-VC and Micro-VC funds have grown the most, with more funding rounds, but represent the least amount of assets under management, between 2008 to 2018. We next introduce and explain the factors that can support venture capital firms, at least those in Nano-VC and Micro-VC, raise funds.

Figure 8: Distribution of US Venture Capital Fund Sizes: By Total Number of Funds (Left) and Total AUM (Right)

Source: Toptal

Now we discuss how Venture Capital Emerging Fund Managers can raise funds, or atleast increase their chances of raising a fund successfully. First, utilising social media such as Twitter, helps. However, Emerging Fund Managers with those that have a BAME or women based team, or experienced but small team, are likely to succeed, as discussed earlier, therefore can utilise social media to gain funds which was evident in our subheading ‘Fund Managers’.

When you solicit publicly, you need to make sure that you are classified correctly. According to the SEC , Rule 506(c) permits issuers to broadly solicit and generally advertise an offering, provided that:

all purchasers in the offering are accredited investors

the issuer takes reasonable steps to verify purchasers’ accredited investor status and

certain other conditions in Regulation D are satisfied

We saw that when defining Emerging Fund Managers, there is no one definition, so to attain the right funds, Emerging Fund Managers need to know their ultimate goal, and therefore their target audience, and then choose the right marketing approach – social media or not. This will ensure Emerging Fund Managers in VC receive the funds they want or need, which in turn can help with the fund performance. Note in later sections, when we mention VC receive the right funding, we then expect fund performance to generate strong returns. Second, having a differentiated investment strategy, helps. We discussed a differentiated investment strategy that generates return, but provides a competitive advantage that can increase the chances of success. Venture Capitalists that can generate successful returns are attractive, which in turn will help VC receive the right funding. Third, effective relationships with limited partners.

Figure 9: Statistics on those raising their first fund

Source: InsightforEmergingFundManagers

Figure 10: Biggest challenge when raising a fund

Source: InsightforEmergingFundManagers

Types of LPs (breakout)

Source: Adobeindd

Covid

Covid has placed a few strains in the Emerging Fund Managers ability to raise funds. There have been many challenges, but we focus on one key area. We noted that investors care most about the relationship between a fund and a LP. The pandemic increased the difficulty for limited partners to invest in Fund Managers, particularly since it is difficult for LPs to meet managers, while also LPs investing in managers they never met face to face, putting a halt on an effective relationship between managers and LP, which in turn reduces investors willingness to invest in a fund, but overall fund performance.

On the other hand, there has been a positive change in the industry. The pandemic has raised the importance of BAME and/or female managers, indirectly, and the need for BAME and/or female managers to manage smaller funds. This is because there is a stronger need for equitable allocation of capital, with the pandemic adding liquidity challenges, and unconscious bias leading to investment decisions, unbiased investment decisions particularly driven by BAME and/or female managers can ensure better allocation of capital and solving the liquidity challenge imposed by the pandemic. With diversified-owned firms representing total AUM across all asset classes at 1.3%, we can see a change with Diverse Fund Managers growing, but also Emerging Fund Managers being diverse, as the two fields are distinct as mentioned earlier. What this could mean, and increasingly likely to be the case, is fund performance improving through diverse Emerging Fund Managers, and investors seeking diverse EMerging Fund Managers.

Touching thoughts:

Emerging Fund Performance can be influenced by many factors, but the most important is the role of a limited partner. Similarly, investors seek funds of a firm that are characterised with a strong relationship, between an LP and a GP. What can be concluded is that for Emerging Fund Management, the role of a LP is crucial. Next, future reports should focus on the role of diverse Emerging Fund Managers as it is a growing topic, which was not covered in detail in this report.

DISCLAIMER:

Any and all communication before, during, and after this event is not to be construed as legal, financial, or tax advice and is for informational and educational purposes only. It is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Sutton Capital Holdings Corporation, Sutton Capital Advisors, and Sutton Capital Ventures I LP makes no representations and gives no warranties of whatever nature in respect of these documents, including but not limited to the accuracy or completeness of any information, facts and/or opinions contained therein.